Cary’s Media Kit

Cary’s Books

Looking for something?

Skip to primary navigation

Skip to main content

Skip to footer

Home

About Cary

The Money Queens Guide

Cary’s Awards

Speaking

Cary’s Speaking Engagements

Consulting

Media

Press

TV

Articles

Podcast & Radio

Blog

Contact Cary

Cary Carbonaro

For Women Who Want to Build Wealth and Banish Fear

About Cary

The Money Queens Guide

Women & Wealth

Cary’s Awards

Speaking

Consulting

Media

TV

Articles

Podcast & Radio

Cary’s Media Kit

Press

Blog

Contact Cary

Cary's Blogs

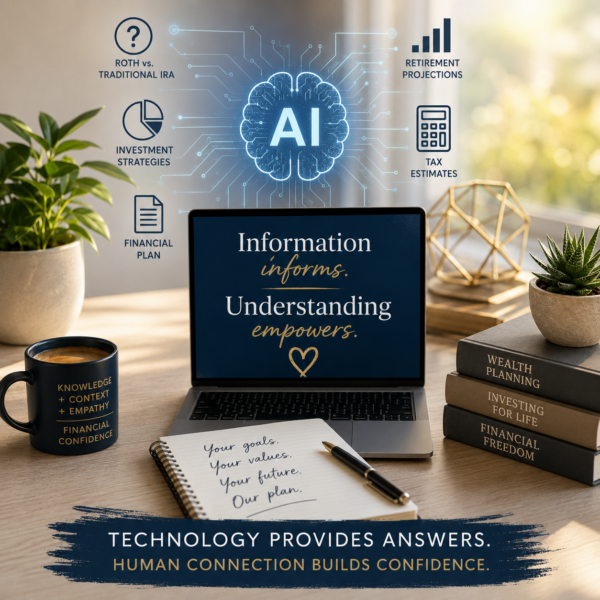

AI Can Give Women Financial Information. It Cannot Give Them Financial Confidence

Spousal Benefits and Other Social Security Decisions Clients Need Help With

When Divorce Happens, Financial Power Matters

Midlife Money Check: Is Your Retirement Plan on Track, Gen X?

5 reasons 2026 will be the year of the woman client

A Trillion-Dollar Opportunity Advisors Can’t Ignore

How to Attract and Retain Female Clients

Advisors Can Help Close the Women’s Wealth Gap

The CFP Board Mission to Argentina: A Deep Dive into Economic Reform and Global Markets

Living the Taylor Swift Economy: A Priceless Night in Toronto with My Niece

Thoughtful Giving: Financial Planning for Maximizing Giving Back

Happily Ever After: Help Women Write Their Own Future

How to Protect Clients from ‘Tinder Swindlers’

KEY CONSIDERATIONS FOR A WARM WEATHER RETIREMENT MOVE

How I Use Fear to Make Positive Financial Decisions

Page

1

Page

2

Page

3

Page

4

Next

→